Why Falling Active Addresses Signal Structural Cooling, Not Just a Lull

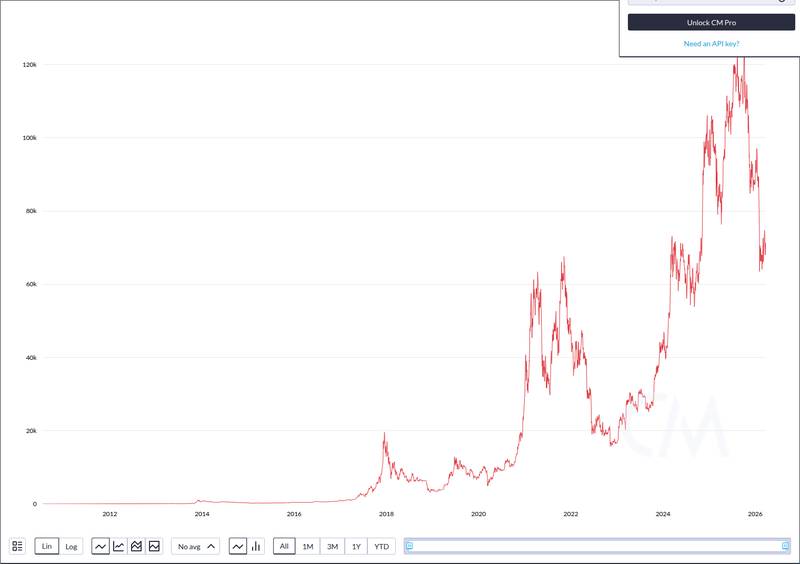

Periods of declining active addresses have occurred before in Bitcoin’s history, and their significance depends on context. During the 2022 bear market, active addresses fell alongside price, reflecting broad capitulation. In contrast, the current drop is happening while price remains elevated, a pattern more consistent with fading retail interest and reduced speculative turnover.

One corroborating signal: spot Bitcoin ETF flows have also turned negative. ETF products have seen billions in outflows during the same period that on-chain activity has weakened. When both on-chain participation and institutional product demand soften simultaneously, it suggests the cooling is not limited to one segment of the market.

The word “structural” matters here. A routine weekend dip in addresses or a holiday slowdown recovers within days. A 30%+ decline sustained over weeks, accompanied by falling new address creation rates, points to a broader contraction in network demand.

Some analysts have reframed the decline more optimistically, suggesting that falling active addresses during price stability could indicate an accumulation phase. In this reading, weak hands are exiting while long-term holders absorb supply quietly, setting up a tighter supply dynamic for the next demand impulse.

Both interpretations acknowledge the same underlying data. The disagreement is about what comes next, not about whether network participation has meaningfully declined.

What On-Chain Participants and Analysts Are Watching Next

For the cooling thesis to be invalidated, active address counts would need to recover above the levels seen at the start of 2026. Historically, sustained recoveries in this metric have preceded or accompanied renewed price momentum, while continued declines at these levels have preceded extended consolidation or drawdowns.

The one-year low in active addresses is a specific threshold to monitor. If daily active addresses stabilize and begin climbing back from current levels, it would suggest new demand is entering the network. If the metric continues to drift lower, it would reinforce the structural cooling narrative.

Several catalysts could shift participation in either direction. The ongoing effects of the 2024 halving continue to tighten new supply issuance, which can amplify price moves when demand returns. ETF flow reversals, should they materialize, would likely show up in on-chain data as increased address activity within days.

Exchange reserve trends provide an additional data point worth tracking alongside active addresses. Declining exchange reserves paired with low active addresses would strengthen the accumulation thesis. Rising reserves paired with low activity would suggest holders are positioning to sell into any recovery.

The current active address levels sit closer to cycle-low norms than mid-cycle norms, based on historical comparisons. That positioning does not guarantee a bottom, but it does narrow the range of likely outcomes. Either participation recovers from these depressed levels as it has in prior cycles, or the metric is resetting to a new baseline that reflects a structurally different Bitcoin market shaped by ETFs and institutional custody.

The next meaningful data point arrives with the monthly close. Whether active addresses hold at current levels or break lower through the end of March will help determine if Bitcoin’s internal cooling is a temporary repricing of participation or the early stage of a deeper demand contraction.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency and digital asset markets carry significant risk. Always do your own research before making decisions.